Last Updated on August 3, 2023 by Ashley Poynter

As we move into 2020, questions remain around the state of payments both in the U.S. and abroad. Innovation and disruptive changes have ushered in a transition period from traditional to digital, but both businesses and consumers are waiting to see how some of these changes will shake out. Consolidation was the name of the game in 2019 — and may continue to steal headlines in 2020. I spoke to the experts to uncover thoughts and predictions for the payments landscape in the coming year.

This is the fifth in a series of Payments & Fintech Q&A articles featuring thought leaders in the space (You can view the first here, the second here, the third here, and the fourth here). Stephanie Foster launched a stellar career in financial technology nearly two decades ago at Western Union. Today she serves as a Payments Product Leader at Fiserv. Stephanie holds a number of Industry accolades: Money 20/20 Rise Up Class of 2018 and Electronic Transaction Association’s (ETA) Forty Under 40 for 2019. As part of her commitment to strengthening diversity and inclusion in FinTech, Stephanie helped found Women Driving Innovation in Atlanta with the mission to connect, inspire and empower the next generation of female thought leaders in tech. She also serves as a member of the Women’s Network in Electronic Transactions’ (Wnet) Advisory Board.

Ashley: What is your “big prediction” for Payments in 2020? Who will the big players be? Also, what technology/(ies) will lead the headlines in transforming payments as we know it?

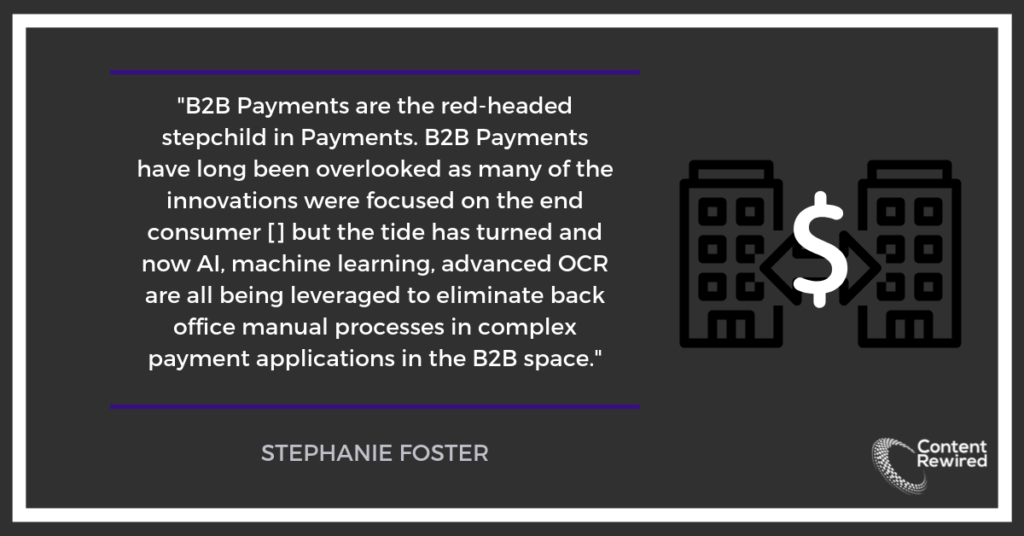

Stephanie Foster: I’d like to answer this from the B2B perspective. B2B Payments are the red-headed stepchild in Payments. B2B payments have long been overlooked as many of the innovations were focused on the end consumer (i.e. Online billpay, ApplePay, Zelle, etc…) but the tide has turned and now AI, machine learning, advanced OCR are all being leveraged to eliminate back office manual processes in complex payment applications in the B2B space. I foresee banks and fintechs continuing to innovate to provide more efficiencies in B2B Payments from EIPP (Electronic Invoice Presentment and Payment) portal options to integrated receivables/invoice to cash automation. Electronic payments will continue to rise as per a 2016 NACHA ACH study, 70% of corporates stated they were likely to convert their payments to electronic within 3 years.

Ashley: By next year, 40% of US consumers will be made up of Gen Z. How will this impact digital payments trends as well as how financial institutions respond to changing consumer demands?

Stephanie: Gen Z grew up with the internet and they have never known life without it. E-wallet and social media play a big part in how and where they shop. Quick, easy, seamless transactions are key. Gen Z is the “connected” generation seeking connected experiences through voice and mobile in all parts of their lives.

Additionally, they care about the environment and social causes so opportunities to give back to an important cause drives their decision-making in spending their dollars. This will create an uptake on digital payments in the next 5 years. Financial institutions must focus on the user experience of their Gen Z consumers in order to earn their trust and loyalty. The name of the game is value, speed and convenience.

Ashley: With PSD2 coming into full effect for the EU next month, many wonder if open banking will make its way to the US. What are your thoughts on this? Are there benefits to the US adopting an open banking model?

Stephanie: Call me a skeptic but Open Banking will not be making its way to the US any time soon. Think about the recent data breaches — Equifax — that has resulted in 147 million consumers impacted and a fine of a settlement with the Federal Trade Commission up to $425M. Capital One — 100 million consumers’ personal data compromised due to a breach conducted by one individual. I am not convinced that US regulators, banks and consumers are prepared to allow companies like the Amazons of the world to retrieve consumer bank account data to facilitate payments.

As a “ Payments Geek” and millennial I am looking forward to Open Banking on our side of the world as it is one more way to empower consumers by providing access to manage money, borrow money, invest money easily, safely and securely. Who wouldn’t want that? Imagine the ability to view all of your financial accounts from ONE single platform on your phone? Mint, the budgeting platform is a pioneer in this space but it remains to be seen how the regulators will react. The possibilities are endless!

Stay tuned in the coming weeks. I will be interviewing more experts on the evolution of the payments world, shifts in the ecosystem, and what to expect in 2020.

If you’re interested in participating in one of our Q&A With the Experts series, please send us a note here.